Hurricane Helene's havoc has exposed major gaps in U.S. flood insurance

Hurricane Helene's havoc has exposed major gaps in U.S. flood insurance

As human-caused climate change fuels flood risks.

Hello —

Scientists at the Lawrence Berkeley National Laboratory have calculated that during Hurricane Helene, human-caused climate change may have caused as much as 50% more rainfall in some parts of Georgia and the Carolinas. Helene is now considered “the deadliest mainland U.S. hurricane since Katrina.”

Find out more at Yale Climate Connections about how climate change made Hurricane Helene more severe

Hurricane Helene is likely the 21st billion-dollar disaster to hit the U.S. this year alone. AccuWeather estimates find that total damages and economic losses could reach $160 billion.

This tragedy isn’t a natural disaster; it’s a systemic failure that left families without proper evacuation warning, emergency support, and now adequate insurance to recover.

Only 2% of households in the parts of Georgia, North Carolina1, and South Carolina where flooding was caused by Hurricane Helene have federal flood insurance. This highlights the major gaps in U.S. flood insurance as climate change amplifies flood risks.

The National Flood Insurance Program is not financially solvent and is over $20 billion in debt. According to the Congressional Budget Office (CBO), flood insurance rates will double in the coming years, with some rates increasing by more than 300%.

Risky business

No place is safe in this new era of climate disasters. This catastrophe isn’t just about one storm—it’s a reflection of deep-rooted vulnerabilities in U.S. housing policies, insurance markets, and disaster response systems. Climate change impacts all regions of this country. It has hit regions not typically associated with climate impacts, like Eastern Tennessee and Augusta, GA region, and even Asheville, North Carolina, once hailed a “climate haven.” This storm demonstrates that we need a national response.

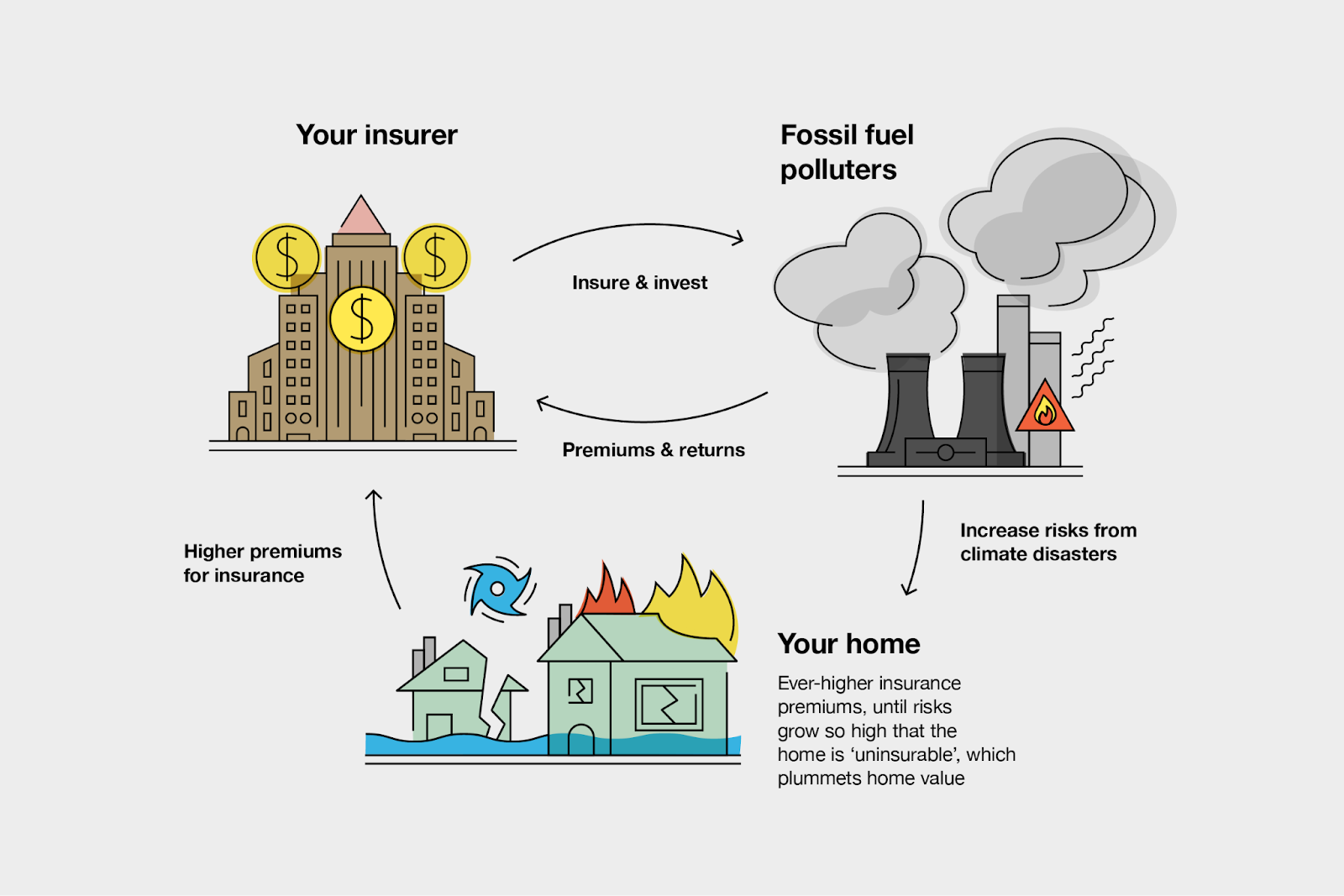

Fossil fuel-driven climate change will continue to exacerbate extreme weather disasters, and as insurers hike premiums, limit coverage, or leave markets, Americans are left unprotected in their time of greatest need.

U.S. insurers invest billions in fossil fuel companies and continue to underwrite harmful fossil fuel infrastructure while blaming climate change for coverage loss or premium hikes. Insurers must divest from the root cause of climate change in order to solve the uninsurability crisis.

Towards solutions

People and communities continue to suffer from deadly and costly fossil fuel-driven disasters while officials are failing to hold insurers and fossil fuel corporations accountable. What is to be done?

Widespread insurance industry reforms and pressure on government officials, particularly state insurance commissioners, are needed to ensure a more stable insurance market with better protections.

The absence of federal insurance regulation has led to an opaque, fragmented array of state policies, with some states enabling insurers to exacerbate climate change and leave citizens vulnerable. This needs to change! A new report from the Climate & Community Institute (CCI) recommends establishing state or federal Housing Resilience Agencies (HRAs) to provide public disaster insurance and coordinate community-focused disaster risk reduction. The report calls on officials to address market gaps by covering underserved sectors like multi-family housing, renters, and mobile homes, while promoting transparency through public risk models and diverse advisory councils. View the webinar discussion here.

Make the polluters pay! Vermont passed a law requiring fossil fuel companies to pay for climate damage and Connecticut advanced similar legislation to hold insurers of fossil fuel projects accountable. Legislation in New York is also being considered that would protect communities from the twofold problem of predatory insurance practices and the worsening climate crisis.

Here is Green America’s directory of climate smart insurance companies.

Dive deeper

Helene Should Trigger a National Rethink of Home Insurance (The New Republic)

Democrats Must Start Distinguishing Themselves on Insurance Policy (Prospect)

‘It’s going to be a mess’: The flood insurance crisis following Helene’s wreckage (Politico)

Nowhere in America Is Safe From Climate-Fueled Storms and Fires (Bloomberg)

US Flood Insurance Program Faces an Increase in Repeat Payouts (Bloomberg)

Insuring the Climate Crisis: New Bill Aims to Rein in Predatory Insurance Practices (CIEL)

Florida politicians’ climate denial draws destructive response from Helene (commentary by Craig Pittman for the Florida Phoenix)

Hurricanes are dangerous far from the coast. Communities are struggling to prepare (NPR)

With thanks to the folks at Petkanas Strategies and Americans for Financial Reform for passing on these resources!

This is so important, thanks for highlighting this complex topic. The irony of our home insurance premiums being invested to further fossil fuel development and production is obscene and should lead to action. This summer organized protests addressed this and more https://www.summerofheat.org/

The recovery of housing from disasters has many aspects in addition to insurance coverage. I learned this when working to recover from the 1994 Northridge earthquake in Los Angeles when thousands of Angelenos, mostly renters, were displaced from their homes. Most communities pay little attention to disaster housing planning until experience teaches them its importance. Hurricane Katrina reminded us of this fact after all the attention and money was going to terrorism-related work. Progress has been made but we have a long way to go.